Pricing Strategies for Solicitors: Maximising Fees with New and Existing Clients

The legal profession has changed dramatically over the last few decades. Clients are increasingly discerning, better informed, and, in many cases, expecting more transparency about the fees they pay. Traditional methods of billing by the hour still exist, but there is growing acceptance that fixed-fee value-based pricing is both beneficial and ethical for solicitors and clients alike. By focusing on what clients truly need and the outcomes you help them achieve, you can set fees that reflect your value rather than just the time spent on a matter.

Below, I’ll explore two dimensions of successful pricing for solicitors and law firms. First, I’ll look at how to achieve the best price when taking on new clients. Second, I’ll examine how to negotiate (and where appropriate, raise) your fees with existing clients.

Achieving the Best Price with a New Client

Step 1 - You need to embrace a value-based mindset.

Far too many professional services, including solicitors, start by asking, “How many hours will this matter require?” and “What is the relevant hourly rate?” Instead, the key is to ask, “What is the result the client is seeking, and what is that result worth to them?” Clients ultimately care about the outcome.

If you can translate your advice and support into tangible and intangible benefits for them, you shift the discussion from “hours and tasks” to “value and transformation.”

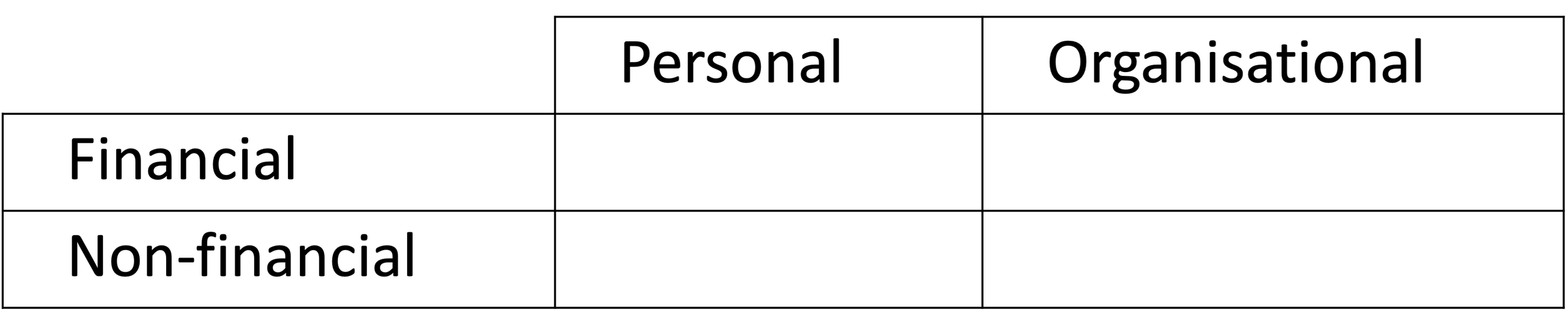

When doing this, there are two dimensions to consider – the type of benefit, and who benefits. Think of a 2x2 matrix which looks like this:

Some areas of the law only concern personal / non-financial benefits – for example, if your client seeks help with child custody. Others, such as a commercial contract negotiation, can involve all four aspects. Imagine the General Manager of a UK subsidiary involved in contract negotiations with a customer, and they want the best terms possible:

Financial / Organisational – benefits might include maximising the value of the contract

Non-financial / Organisational – positive PR following a successful negotiation which helps to attract new talent into the organisation

Financial / Personal – a good outcome could lead to promotion and a bonus

Non-financial / Personal – minimising risk to reputation

The point is to consider all the possible types of benefit to the client.

Focus on outcomes, not tasks. For instance, if you are advising a business client on a restructuring, do not simply list the tasks (drafting documents, attending meetings, etc.). Instead, highlight the end state: moving to a lower-tax location, selling part of the business in a trade sale, etc. Emphasise how your unique advice and interventions will significantly reduce risk or increase the likelihood of a positive outcome.

Determine the client’s need behind the request. Sometimes, what clients initially present is not their real issue. Probe deeper: ask why they are seeking a particular service. It may turn out that solving a bigger or adjacent problem is more valuable and allows you to justify a higher (yet fair) fee.

Step 2 - Next, before quoting any figure, examine three fundamental questions:

Fit? Why are you the best person to work on this? Perhaps you have unique expertise in a niche area of law, a proven track record in a particular industry, or a well-known reputation for winning similar cases. If you can demonstrate that you are either the authority or at least the most trusted figure in their specific context, the client will happily pay more for peace of mind.

Timing? Identify any pressing deadlines, regulatory changes, or windows of opportunity. If your client genuinely needs immediate action - for instance, to prevent further losses or to exploit a short-term market opening - this urgency supports the logic for a robust fee.

Approach? Do things have to be done a particular way? Determine why they have not done this work internally or engaged a cheaper alternative. Some tasks (like litigation or specialised commercial drafting) require expertise that smaller in-house teams simply do not have. If a client has tried other solicitors but achieved poor outcomes, emphasise how your approach is different.

Step 3 – Then you should develop a clear mutual understanding of objectives. When you sit down with the prospective client (the true decision-maker, not an intermediary), agree on:

Objectives: What precisely do they want to accomplish?

Measures of Success: How will you both track progress? It may be financial (e.g., damages avoided, value of sale), or qualitative (e.g., brand reputation defended, management time freed up).

Value to the Client: Encourage the client to articulate the benefit in their own words. This might involve protecting their intellectual property, preserving a legacy, or obtaining swift closure on a family dispute.

Putting a clear value on the outcomes (financial or otherwise) ensures they appreciate the significance of your contribution. Once that value is firmly established, the subsequent fee discussion feels fair and proportionate.

Step 4 – Decide how to present the fee.

It is often beneficial to present more than one fee option – Price Relativity. For instance:

Option A: The essential service that meets their core objectives.

Option B: An enhanced service that adds a layer of support (e.g., additional legal opinions, training for in-house teams, or ongoing reviews).

Option C: A premium service that offers maximum assurance and might include 24/7 availability for urgent queries, the drafting of a comprehensive set of policies, or a full multi-jurisdictional strategy.

Each option should have a distinct outcome and fee. This allows the client to weigh the importance of extra reassurance and scope. Crucially, never present these options as simply more hours of work. They must be presented in terms of increased value and reduced risk for the client.

In addition, if you do present more than one option, start with the highest price first – that creates an anchor. The first price becomes the reference against which the next two options are compared.

Finally, make the fees precise. An exact fee suggests that there is some science behind how it was calculated, and it is less likely to be negotiated down.

Step 5 – Budget discussions

There is an advantage to being the first to mention a number. It creates an anchor, and negotiations are then up or down from that number. If you ask the client about their budget and it is unrealistically low, it is a difficult conversation to get it back up to an appropriate fee level.

Instead, it is better to indicate what your anticipated fee will be, even if it is approximate before you then communicate in your proposal what the exact fee will be.

Negotiating and Raising Fees with Existing Clients

Existing clients can be both easier and more challenging when it comes to pricing. On the one hand, they already know and trust you. On the other, they may have expectations based on older, possibly under-valued fee structures.

Option 1 – Make sure you are selling value

If your legacy clients are still paying by the hour, you could be leaving money on the table - and potentially devaluing your expertise. Shifting to a more value-based model can benefit both parties:

Explain the Benefits: Emphasise that value-based fees shift the focus from ticking hours to achieving outcomes. This arrangement incentivises you to be efficient, creative, and proactive, rather than simply “clock-watching.”

Stress Peace of Mind: Under a fixed or value-based fee, clients can budget more accurately and need not worry about mounting hours. You assume the risk of inefficiency, which many clients appreciate.

Offer Structured Packages: For instance, propose a retainer covering unlimited phone advice or quick email consultations. Make clear that any extensive project (like drafting a new set of contracts or significant legal research) would be proposed and billed separately.

Option 2 – Managing scope creep and fee creep

Let’s define the two terms.

Scope creep is where the project expands based on client requests. For example, the client asks for little things which individually seem reasonable but which, by the end of the project, add up to significant additional work.

Fee creep is where the scope has been agreed with the client, but there is a desire to overdeliver, and you end up needing to either write off extra work or there is an uncomfortable conversation with the client about work they didn’t really ask for.

There are two parts to resolving this.

First, and most importantly, is the need to regularly (preferably weekly) communicate progress to the client. There should be no surprises at the completion of the matter.

Second, when the client requests additional work, quote for it: “I’m very happy to assist with that, but it does extend beyond our original agreement. Let me draft a short addendum reflecting the new scope and investment.”

Option 3 - Finding New Circumstances for Fee Adjustments

Existing clients often present fresh opportunities for expanded or renegotiated engagements. Look for the following trigger points:

New Leadership: If a new CEO or department head arrives, it can be an excellent time to propose a broader arrangement or different fee structure.

Strategic Shifts: If the client is entering new markets, launching products, or restructuring, highlight how you can assist proactively in multiple areas - and propose a retainer that covers broader counsel rather than single-issue billing.

Year-End Budgeting: Many organisations need to allocate budgets before the financial year ends. If there is available budget that they risk losing, propose an annual or multi-month retainer that secures your services for the coming period.

Option 4 - Handling Fee Increases

Raising fees for clients who have grown accustomed to a certain rate can be delicate. Yet, if your expertise has grown, or if the complexity of the client’s matters has increased, it is only fair to adjust fees accordingly. Here are some tips:

Demonstrate Continuous Value: Show your client how you have contributed to their successes or protected them from significant losses over the past year(s). Highlight intangible benefits such as convenience, peace of mind, and quicker turnaround times.

Give Notice: If you are raising retainer fees or shifting away from hourly billing, provide a transparent timeline. For instance, you might say: “From the start of the next quarter, our new retainer fee will be…”

Provide Options: As with new clients, consider offering multiple tiers. The higher tier might include expanded services or top-priority scheduling, while the base tier covers essentials.

In addition, just because a client knows you well does not mean they fully understand the breadth of your capabilities. Take the initiative to:

Offer Additional Services: If you spot that they could use help in an area you have not previously handled - perhaps employment law or compliance - mention it.

Arrange Check-Ins: Schedule periodic reviews where you both evaluate the progress of current matters and consider upcoming objectives. These discussions are ideal moments to introduce any new fee arrangements or additional services.

Option 5 - Walking Away if Necessary

Sometimes, an existing client is simply unwilling to recognise your increased value or the evolving complexity of their needs. They may insist that the original fee structure (perhaps even the original rate from five years ago) continue indefinitely. In these rare cases, it may be in your best interest to conclude the relationship.